Here’s how I manage my finances in 2025. I plan to publish an updated version each year. As always, consult a financial planner before making changes to your approach. (Some of the links below are affiliate links.)

Banking

I recently moved my chequing and savings accounts from Simplii Financial and EQ Bank to Wealthsimple. I receive a 2.75% interest rate on my accounts because I automatically deposit my paycheque, and my wife and I are Premium members. It’s fairly quick to reach premium status if you join forces with someone who shares the same residential address.

Being a Premium member offers many benefits. I chose to get access to Uber One, while my wife chose to get Strava for free.

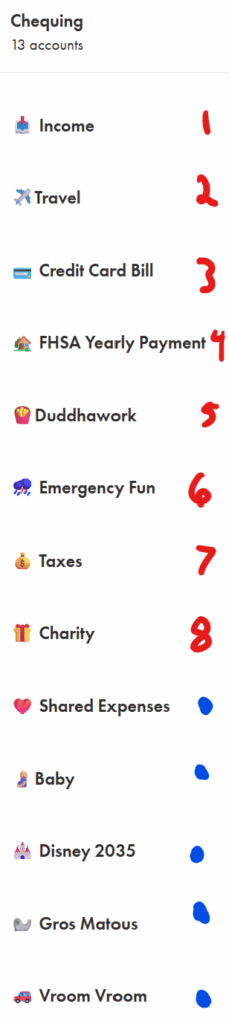

I love that I can open up to 8 individual chequing accounts, and open or join up to 8 joint chequing accounts. I deposit my paycheque into a chequing account labeled ‘Income.’ From there, I automatically distribute money to my sub-savings accounts the day after I receive my paycheque.

For example, I save $50 towards Travel every two weeks. It’s nice to plan a trip knowing that you have $3000 ready to be spent without guilt.

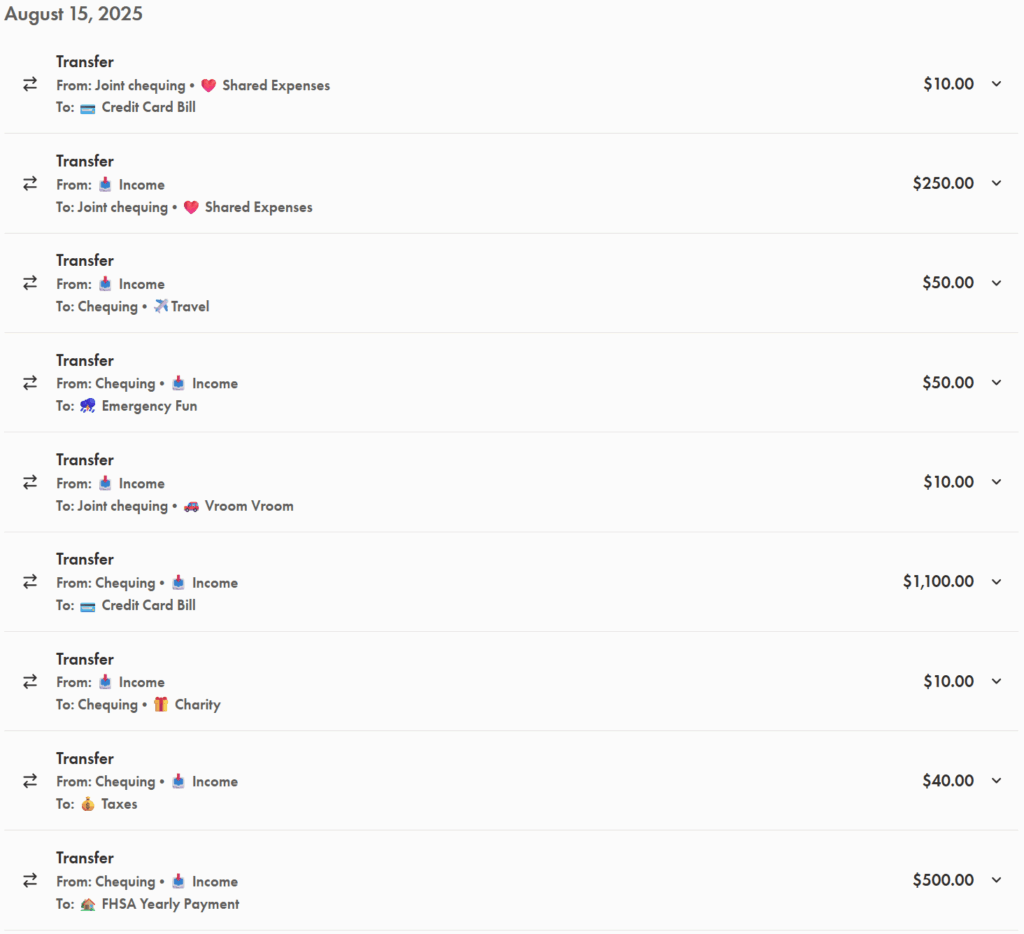

I automatically put $1100 aside every paycheque in an account called Credit Card Bill. It’s from this account that I pay my credit cards once I receive my statement. This allows me to build credit, benefit from rewards, without having to stress about not being able to pay my bill at the end of the month. I pay my Rent with my Scotia Momentum Visa Infinite Card through Chexy. Tracking my credit card expenses allowed me to determine that saving $1100 is usually enough to pay the bills. It’s great that Wealthsimple allows you to pay bills and e-transfer from any account without having to transfer money from your savings accounts to your chequing account to avoid transaction fees.

I also save aggressively towards buying a House by putting aside $500 per paycheque. I use this account to accumulate money that can be deposited in my FHSA, TFSA, and RRSP at the start of the next year. That way, I can max out my FHSA and TFSA in the first week of January, which simplifies keeping track of my contribution room. I’ve yet to max out my RRSP, but I plan to use it through the Home Buyers’ Plan.

I have a separate account for my Business where all those income streams are automatically deposited.

I have an Emergency Fund of approximately $7,000. I continue to contribute $50 per paycheque to it until I reach about $10,000. I plan to supplement this emergency fund by adding a Wealthsimple line of credit.

I sometimes owe Tax money at the end of the year, so I save $40 per paycheque to avoid a big surprise.

I started saving $10 per paycheque towards Charity. I plan to increase this amount as my income increases. Having a separate account dedicated to charity encourages me to support local fund raisers and donate to the causes I believe in. I’d love to eventually give a yearly bursary of $500 to graduating high school students.

My wife and I both contribute $250 every two weeks towards Shared Expenses. We transfer money from this account to our personal accounts when one of us pays for groceries, gas, or utilities, for example.

We both contribute $10 to a Car fund. We could simply increase our contribution to the shared expenses account, but I like having a separate account for the car because its expenses are rare and hard to predict. It works as a mini emergency fund specifically for the car. It doesn’t make sense to dip into your main emergency fund for predictable but irregular car expenses.

What I love about this system is that every account has a bit of buffer space, which helps you sleep at night. It’s great that there are no fees and minimum balances, but the competitive interest rate helps you reach your goals. The monthly interest I receive in my emergency fund is a meaningful boost to my savings.

It’s crucial to note that for this system to work, you need to earn more than you spend. I currently auto-save $2020 per paycheque, which is slightly higher than my full post-tax teacher paycheque. This incentivizes me to make up the difference with my side hustles. I can tutor, teach summer courses, take on random contracts, and have a summer job. I can always lower my savings rate if there’s too much pressure in the system.

Credit Cards

I’ve established this 4-credit card system based on our current spending patterns.

| Area | Credit Card | Rate |

| Recurring payments Rent | SCOTIABANK Momentum Visa Infinite | 4% |

| Groceries | SCOTIABANK Momentum Visa Infinite | 4% |

| Restaurants Bars Coffee shops | SIMPLII Financial Cash Back Visa | 4% |

| Travel Abroad | Wealthsimple | 2% + No Fx Fees |

| Everything Else (including Costco) | Rogers Red World Elite® Mastercard® | 2% (3% if redeemed with Rogers, Fido or Shaw) |

I recently switched phone plans to join Fido and reduce my monthly bill. This allows me to earn 3% cashback on all purchases, including Costco. I even earn cashback on rent through Chexy. All cards are free except the Scotiabank card, with an annual fee of $120. The fee was waived for the first year, and paying my rent with Chexy more than pays for it. I’ll cancel this card once we buy a house if Chexy isn’t an option for mortgage payments.

Some cards, such as the American Express series, might offer more rewards if the points are redeemed as travel miles. That said, I find these cards encourage spending and add complexity to the system. My system fits my current lifestyle and values. I’ll have to adjust it if I start travelling for work or when we have kids.

Taxes

We complete our taxes with the free Wealthsimple Tax software. We get free audit protection as premium clients, and we’ll get free advice when we reach the Generation tier. It’s relatively simple to do, especially if you don’t have a complicated financial life.

Mortgage

We don’t have one yet, but we plan on going with Pine. Please reach out if you know better options.

Life Insurance

I get a complimentary 3X salary life insurance through my work. I’ll get term insurance for about 1 million dollars once we’re expecting our first child. I plan to keep this insurance for the time our children are vulnerable, which should be about 20 years.

Here’s what Policyme says:

This would amount to paying 12 to 15K over the 20 years, which is nothing to sleep peacefully knowing that my family is taken care of.

Will

We both updated our wills after getting married. Every Canadian should have a will. One of the premium benefits of Wealthsimple is to get a free will through Willful. We used a local lawyer, though online options are cheaper.

Pension

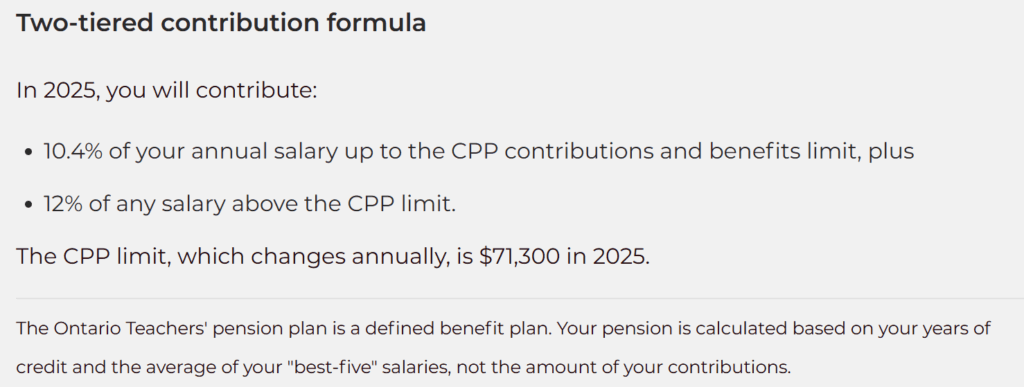

I teach high school math full-time in Ottawa, Canada. About 10% of my pay goes towards my pension.

I currently earn $80,592.46 per year and thus contribute 0.104*71300 + 0.12*(80592.46-71300) = $8,530.30 yearly.

Contributions, which are sent to us, are matched dollar for dollar by the Ontario government and participating employers on behalf of all members. Contributions are tax deductible and will be reflected on your T4 slip. While contributions are important, your pension is based on your years of credit (your actual time worked) and average salary, not the amount you contribute. – Ontario Teachers’ Pension Plan

My yearly pension will be 60% of the average salary in my top five earning years. As of now, this amounts to approximately 70K per year for life. This would allow me to retire comfortably.

Investing

Given my pension, CPP, OAS, and that we plan to buy a house, it doesn’t make much sense to delay gratification by investing. Selling the house and downsizing should provide us more than enough money to ball in retirement. Assuming I continue teaching high school, I’m on pace to retire around 56 and earn about 80K until I die. This should be more than enough to live comfortably in Canada, travel, and treat our kids and grandkids once in a while.

Investing in addition to my pension would allow me to supplement my retirement income. That said, making more money in retirement is useless if you can’t take advantage of it. I’ve had unexpected health complications in my twenties that are likely to limit my ability to enjoy travelling in my old age. Hence, it’s rational to invest less and contribute more to my travelling fund. Travelling and paying for experiences like concerts now rather than in retirement makes more sense for me. I’ll get to reap the memory dividends for longer and connect with people who form my social network. In some sense, we retire on our memories and reminiscing. I recommend checking out my Die With Zero book notes to read more on this topic.

Having said that, I still believe in the value of auto-investing some money for retirement. Given my ability, need, and willingness to take risks, I believe that investing in a globally diversified 100% equity ETF like VEQT of XEQT is likely to produce the best return in the long term. I used to invest in VGRO, but I switched to VEQT after doing more research and not panicking when the markets dropped.

Recent research suggests that it might be best to keep this asset allocation even in retirement. This further simplifies our investing strategy: Ride something like VEQT until you die. This cuts through the noise of investing that often paralyzes people.

It’s never been easier to automate investing. Amazingly, any schmuck can automatically buy a basket of the best stocks worldwide with $5 every paycheque. Establishing this habit as early as possible is the key to take advantage of compound interest.

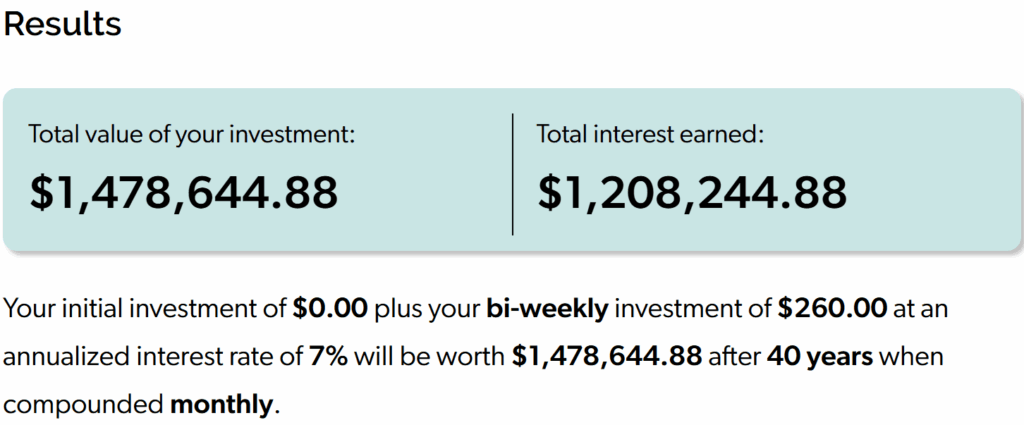

Simply maxing out your TFSA by investing $260 per paycheque from the time you’re 18 to the time you retire at 58 results in roughly 1.5 million dollars that you can pull from tax-free. Compound interest and time gave you 1.2 million dollars for free. That’s the magic of compounding!

Sure, investing $260 bi-weekly may seem like a lot at first, but you can start with $5, build the habit, and work up to bigger amounts. Alternatively, you can always invest 10% of your income regardless of its size.

I invest in VEQT for the long term (30+ years), but I can invest in the lower-risk ETFs for shorter-term goals. For example, I’ve used VCIP and VCNS to invest for buying a house in the next five years. Now that we are closer to pulling the trigger on a home, I invest in cash-alternative ETFs like CSAV.TO. It’s like parking your money in a high-interest savings account. I don’t like GICs for saving for a down payment because it’s impossible to know when the right house is going to come along.

I believe that money is a tool to live out my values. Being broke stops you from being the person you’d like to be. Having a complicated financial system isn’t likely to result in better outcomes. I spend less than an hour per month thinking about my finances. I haven’t been financially stressed in years, even though I’ve been making less than or near the median Canadian income. Use this motivation to take the next step toward financial freedom.

Recommended Financial Resources

Books

- Die with Zero – Notes

- The Psychology of Money – Notes

- I Will Teach You To Be Rich – Notes

- The Millionaire Teacher – Notes

- The Wealthy Barber – Notes

- The Boggleheads’ Guide to Investing – Notes

- Rich Dad Poor Dad – Notes

- Wealthier – Notes

- The Happiness Hypothesis – Notes

- Atomic Habits – Notes

- The Almanack of Naval Ravikant – Notes

- Outlive – Notes

Podcasts

YouTube Channels

Affiliate Links

Read This Next

- Automate Your Finances

- Credit Card Optimization (2025)

- What is your Rich Life?

- Wealthsimple Presents: The End of Banking?

- We Almost Bought a Home

- Our Plan to Purchase a Home

- How I Get 10% Cash Back at Starbucks

- I Finally Switched Phone Plans

- Wealthy Abundance

- I Sold My Bitcoin

- Hindsight Thoughts on Getting Married

- Die with Zero – Book Notes

- Die With Zero – Implementation

- Outlive – Book Summary & Notes

- Millionaire Teacher – Book Notes

- The Wealthy Barber – Book Notes

- Atomic Habits – Book Notes

- The 300 000$ Meeting

- Get To Good Enough & Move On

- Never Buy Shoes That Don’t Fit

- The Parallel Universes of Time and Money

- Build Wealth And Get On With Your Life

- Does it Make Sense to Buy Raffle Tickets?

- What is your Investment Goal?

- What I Learned from Tracking my Mood for 1000 Days

- Stay The Course