Introduction

Kayla and I got married last summer. We’re 29 years old and live in a three-bedroom apartment in Ottawa, Ontario. I’m a high school teacher and she’s a psychotherapist and counsellor. We plan to have children and are contemplating buying a house if and when it makes sense to do so.

We both believe that money is a tool to live a better life. Likewise, we don’t believe that owning a house is a necessary condition for a good life. We’re open to purchasing a house if it aligns with our goals, values, and financial situation. Below are a few options for dream homes for us.

Option 1: Buy a Nice Home in a Nice Neighbourhood

Ideally, we could own a home in a nice neighbourhood. We both don’t want to have to drive to work and value relatively short commutes. I work at Franco-Cité high school and will do my PhD at the University of Ottawa. Kayla works at Ottawa U and her therapy office is downtown. We like to take long walks, work in coffee shops and attend events at Lansdowne, Lebreton Flats, or the Byward Market. The neighbourhoods that best match our values and lifestyle are:

Of course, attractive neighbourhoods result in higher house prices. We can expect to pay between 800K to 1.5 million dollars for a forever home for our family. That is a ton of money. Let’s crunch some numbers to see if it’s even feasible.

Let’s first consider a 1.2 million dollar home.

Down Payment

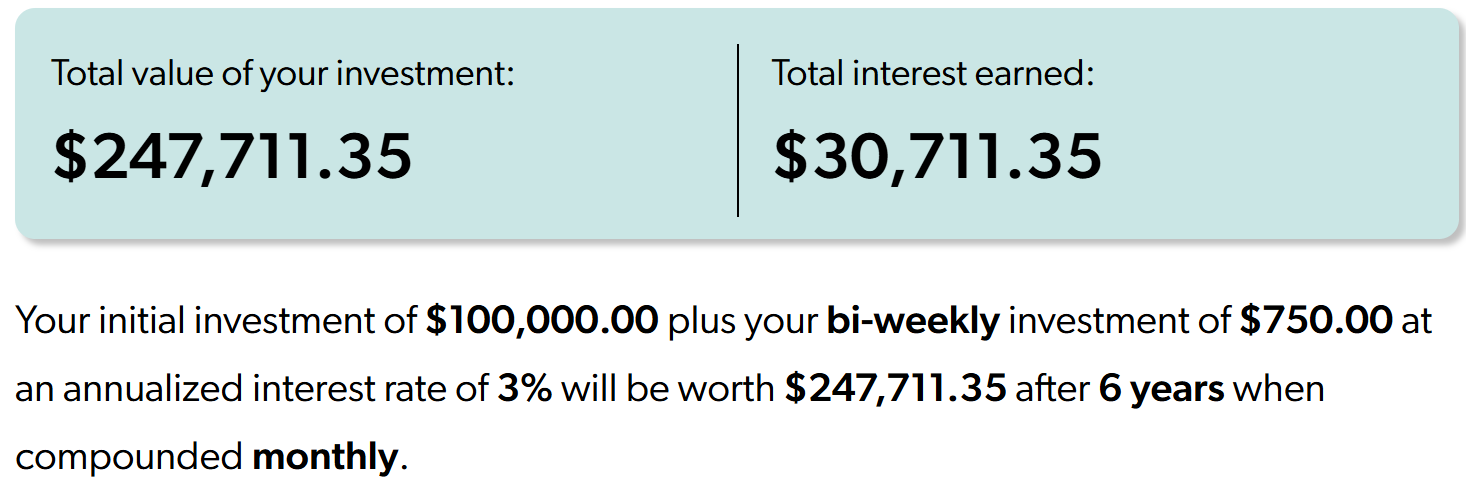

A 20% down payment is 240K. Let’s assume we already have 100K saved for a down and can each save 10K yearly. How long would it take us to reach the 240K milestone? This calculator tells us that we’d each need to save roughly $375 per paycheque for 6 years at 3% interest rates to achieve our goal.

We’ve already built the habit of automated savings so it’s only a matter of deciding which accounts and investments are best suited for saving for a down payment.

Accounts

The FHSA is the perfect saving vehicle for a down payment. The only issue is that the maximum yearly contribution is $8000 for a total maximum of $40,000. Hence, we’ll have to use the TFSA and RRSP according to the schedule below. The Home Buyers’ Plan (HBP) allows us to withdraw from our RRSP to buy or build a qualifying home. The downside of the HBP is that we’ll need to repay what we took out of our RRSPs within 15 years of the house purchase. That is, we’ll each have to contribute roughly $12,000 to our RRSP over 15 years.

| Year | FHSA | TFSA | RRSP | TOTAL |

| 1 | $8,000 | $2,000 | $0 | $10,000 |

| 2 | $8,000 | $2,000 | $0 | $10,000 |

| 3 | $0 | $7,000 | $3,000 | $10,000 |

| 4 | $0 | $7,000 | $3,000 | $10,000 |

| 5 | $0 | $7,000 | $3,000 | $10,000 |

| 6 | $0 | $7,000 | $3,000 | $10,000 |

| TOTAL | $16,000 | $32,000 | $12,000 | $60,000 |

Investments

A Tax-Free Savings Account (TFSA), Registered Retirement Savings Plan (RRSP), and First Home Savings Account (FHSA) are all registered plans that allow us to save for a down while reducing the amount of taxes paid. These accounts act like garages that you can put different types of cars into. Within a TFSA, you can buy a guaranteed investment certificate (GIC), buy individual stocks, or buy a mutual fund which is a basket of stocks. Personally, I want to take the least amount of risk possible to achieve my investment goal. Three tools come to mind:

- GICs (Safe but not flexible)

- Cash-alternative ETFs (Safe but a bit more risky)

- Asset-allocation ETFs (Relatively safe over 6 years but more risky than the options above)

GICs currently offer rates above 3%. However, I don’t like that my money is locked up for a certain amount of time with GICs. Instead, I like to invest in cash-alternative ETFs like CSAV.TO. Depending on my risk tolerance and time horizon for a down payment, I invest in an asset-allocation ETF like VCIP.TO or VCNS.TO. These tools allow me to mindlessly achieve my financial goal while taking the least amount of risk possible.

Mortgage

Now that the down is taken care of, we need to worry about paying for the rest of the house (1.2M – 240K = 960 K). Using this calculator, we get that our mortgage payment would be $5,583.41 per month. I’ve created the following Google Sheets to explore the amortization schedule and run a sensitivity analysis on the interest rates. We can see below how much each payment contributes towards the principal versus how much goes towards the interest.

| Month | Initial | Interest | Payment Amount | Towards Principal | Final |

| 1 | $960,000.00 | $3,958.96 | $5,583.41 | $1,624.45 | $958,375.55 |

| 2 | $958,375.55 | $3,952.26 | $5,583.41 | $1,631.15 | $956,744.40 |

| 3 | $956,744.40 | $3,945.53 | $5,583.41 | $1,637.87 | $955,106.53 |

| 4 | $955,106.53 | $3,938.78 | $5,583.41 | $1,644.63 | $953,461.90 |

| 5 | $953,461.90 | $3,932.00 | $5,583.41 | $1,651.41 | $951,810.49 |

| 6 | $951,810.49 | $3,925.19 | $5,583.41 | $1,658.22 | $950,152.27 |

| 7 | $950,152.27 | $3,918.35 | $5,583.41 | $1,665.06 | $948,487.21 |

| 8 | $948,487.21 | $3,911.48 | $5,583.41 | $1,671.93 | $946,815.28 |

| 9 | $946,815.28 | $3,904.59 | $5,583.41 | $1,678.82 | $945,136.46 |

| 10 | $945,136.46 | $3,897.66 | $5,583.41 | $1,685.75 | $943,450.71 |

| 11 | $943,450.71 | $3,890.71 | $5,583.41 | $1,692.70 | $941,758.01 |

| 12 | $941,758.01 | $3,883.73 | $5,583.41 | $1,699.68 | $940,058.34 |

It’s worth noting that only about a quarter of the first monthly payments count towards the principal. At the end of the 25 years, nearly all the monthly payments will go towards the principal.

The money spent on interest is money gone. For this 1.2M dollar home at 5% over 25 years, we’d end up paying $715,022.36 in interest. If we divide this number by 25, we get that we spent $28,600.89 on interest per year or $2,383.41 on interest per month. The argument that renting is throwing money away is foolish when considering the interest payments. Buying this house is the equivalent of investing $3,200 towards the equity of your home plus paying a rent (interest) of $2,383.41.

A monthly payment of $5583.41 is steep. A rule of thumb is that the mortgage payment should not account for more than 25% of your net income. The net income to satisfy this rule is $134,001.79. This equates to a gross income of over 200K. This is far from my expected salary as a high school teacher. That said, I expect to make close to a gross 100K or net 75K per year in 6 years with summer contracts and other side hustles. My half of the mortgage payments add up to $33,500.46 yearly which would be nearly half of my net income. This is assuming that both Kayla and I will contribute equally and that the interest rates stay around 5%. This is too risky. We don’t want to be house-poor.

This assumes that the interest rate remains around 5% over the 25 years. The table below shows what would happen to the monthly payment for different interest rates. We’re in trouble already at 5%.

| Interest Rate | Monthly Payment | Total Interest Paid | Total House Cost |

| 1% | $3,617.07 | $125,121.91 | $1,325,121.91 |

| 2% | $4,065.13 | $259,539.50 | $1,459,539.50 |

| 3% | $4,543.16 | $402,947.04 | $1,602,947.04 |

| 4% | $5,049.79 | $554,938.19 | $1,754,938.19 |

| 5% | $5,583.41 | $715,022.36 | $1,915,022.36 |

| 6% | $6,142.14 | $882,643.08 | $2,082,643.08 |

| 7% | $6,723.99 | $1,057,197.37 | $2,257,197.37 |

| 8% | $7,326.85 | $1,238,054.75 | $2,438,054.75 |

| 9% | $7,948.58 | $1,424,574.88 | $2,624,574.88 |

| 10% | $8,587.08 | $1,616,123.21 | $2,816,123.21 |

| 15% | $11,963.00 | $2,628,899.57 | $3,828,899.57 |

| 20% | $15,503.46 | $3,691,038.02 | $4,891,038.02 |

One way to make the house purchase work would be to buy a house with a separate rental unit in the basement. That way, tenants could pay between 1K to 2K per month. This might be a good option for multi-generational housing.

Option 2: Rent a Nice Home in a Nice Neighbourhood

Buying a house in Old Ottawa East in the near future isn’t feasible. Another option would be to rent a nice home in a nice neighbourhood instead of buying it. The cost of renting a nice place would be around 4K per month. This is still steep but 4K is realistic for our salaries. We’re currently renting a three-bedroom duplex for $2,700 per month and manage to save for a down. We moved into this place thinking we could raise our children in the first few years of their lives. The extra bedrooms are handy as we both work from home during the summer. One of the offices can be converted into a baby room when the time comes.

Your rent is the maximum you’ll pay. Your mortgage is the minimum you’ll pay.

Ramit Sethi

One advantage of renting is that the rent can only increase by at most 2.5% per year whereas the mortgage payments can double if the interest rates skyrocket. Another advantage of renting is that we are free to move whenever without having to worry about selling costs and so on. Furthermore, we don’t need to worry about unexpected expenses such as a leaky roof or a crack in the foundation. These maintenance costs usually average out to about 1% of the property price per year which is roughly 12K per year. Additionally, we wouldn’t have to pay the property tax.

Ben Felix suggests the 5% rule for deciding whether to buy or rent. Multiplying 1.2M by 5% and dividing by 12 gives us $5000. Indeed, we can rent an equivalent home for less than 5K per month so it makes financial sense to do so. Renting also aligns with our values. I’m ok if I never make a trip to Home Depot.

This New York Times calculator also proposes that renting is advantageous financially.

Option 3: Buy a Nice Home in the Suburbs

A third option is to buy a home in Embrun or Russell. Living in the suburbs could make sense to raise children. Embrun is francophone which is another benefit. The commute to work in Ottawa is roughly 30 minutes with minimal traffic. We could buy a nice home for 750K. Let’s run the numbers for this price to see if it makes more sense.

A 30% down results in 225K which we could save in approximately five years. The monthly payment on a 25-year mortgage is $3,053.43. This amount is reasonable and would give us wiggle room and unexpected events.

The downside of living in the suburbs is that we must commute daily for work or activities. According to Jonathan Haidt and my own research, we adapt to stable external circumstances such as a bigger house, but we don’t adapt well to varying circumstances such as traffic. We both walk or bike to work as a ritual to prepare for and disconnect from work. It automates our exercise. Driving is bad for the wallet, the body, and the planet. Furthermore, relative house size seems more predictive of happiness than absolute house size. We are comparative animals.

People would be happier if they reduced their commuting time, even if it meant living in smaller houses.

Jonathan Haidt

Lastly, the number crunching above assumes that we’d stay in the home for the entirety of the mortgage. Most Canadians move before their mortgage is paid off.

Psychological Factors

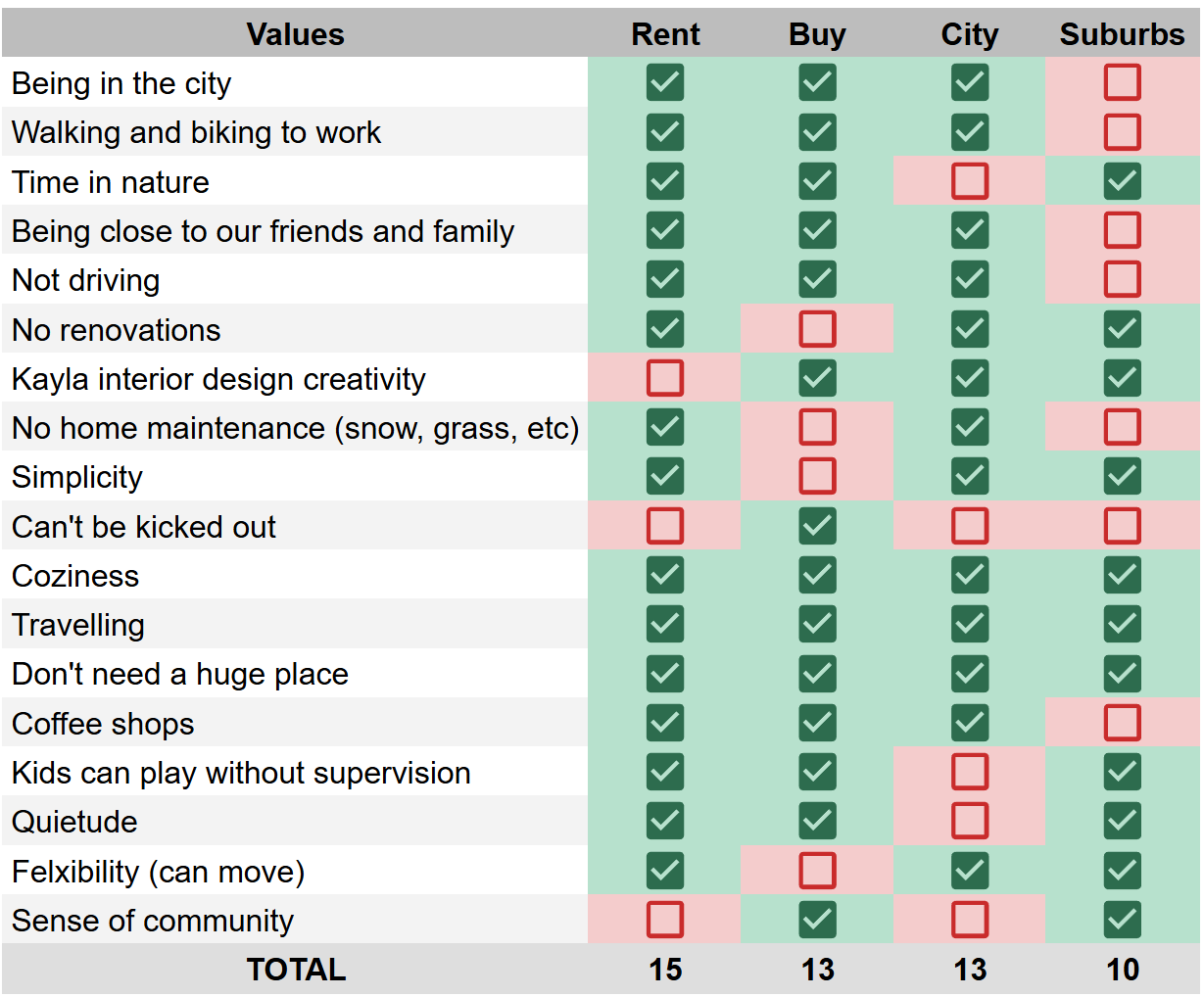

Buying or renting is a personal decision. The main takeaway from this article is that renting is not throwing our money away. It may even be advantageous financially. As a result, the decision boils down to our values and other psychological factors. Below is a non-exhaustive list of our housing-relevant values at this point. There are advantages to both buying and renting while there are perks to living in the city versus living in the suburbs. We both grew up in small towns. Our lives are currently centred around careers and activities, but our values will certainly shift when kids come into our lives.

For people who can’t get themselves to save money, a mortgage can act as a forced savings mechanism. This doesn’t apply to us, however. The ability to have children or work from home would change the calculus. Buying versus renting is a personal decision. Our future selves will have to decide what is best for them and their expected future selves when they have a significant down payment saved.

Read This Next

- Automate Your Finances

- The Happiness Hypothesis – Book Notes

- Die with Zero – Book Notes

- Die With Zero – Implementation

- Gambling versus Calculated Risk-Taking

- The 300 000$ Meeting

- An overarching Theory of Well-Being

- Defining Well-Being

- I Sold My Bitcoin

- Hindsight Thoughts on Getting Married

- Life Score: A Subjectively Objective Way to Evaluate your Life

- What is your Rich Life?

- Build Wealth And Get On With Your Life

- The Wealthy Barber – Book Notes

- What is your Investment Goal?

- Millionaire Teacher – Book Notes

- What I Learned from Tracking my Mood for 1000 Days